INTERNATIONAL INVESTMENT

AND PORTAL

The exchange rate has exceeded VND24,000 per USD due to an interest rate reduction amid a high rise in the US dollar index. Will a continued decrease in the interest rate be a big challenge?

Nguyen Ba Hung, principal country economist at the Asian Development Bank in Vietnam

Nguyen Ba Hung, principal country economist at the Asian Development Bank in Vietnam

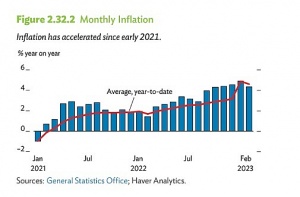

The regulatory interest rate has been reduced four times this year, and it may continue to fall by another 0.5 percentage points. If the policy rate goes down further below the inflation rate, the economy will fall into a situation with a negative real interest rate.

While the policy interest rate is set by the State Bank of Vietnam (SBV), we need to look at the market responses as well, and see whether a decrease in the policy rate will actually reduce lending interest rates in market transactions, and by how much. That is the story of the market and depends on many other factors.

For example, if the lending rate is low but creditworthy businesses do not borrow, the lending rate would depend on the bank’s decision to accept risks of businesses looking for loans, and whether the rate can compensate for such risks. This is essentially a story of supply and demand in the credit market.

Over the past few weeks, we have also witnessed the SBV’s move to absorb liquidity through issuance of State Bank bills. This is a tool to reduce liquidity in the currency market, with one of the reasons being that the banking system has ample liquidity but lending is weak.

Excess liquidity in the system, if not funding credit growth by businesses, could lead to risk of bubbles from stock or real estate speculation.

Market developments have shown that the SBV has been more flexible in monitoring, and with a 28-day term, it could quickly pump money back into the system if liquidity tightened. Meanwhile, the exchange rate still stays within a permissible range, thus not neccessarily being problematic, especially in the context of increasing foreign currency reserves.

What direction should the monetary policy be implemented in the short term?

The actions of authorities have a huge impact on the market. Thus, policy measures need to be predictable for the market to operate stably.

As mentioned, there is still a gap between policy position and market response, and in the current economic situation, the monetary policy alone cannot help the economy achieve high growth.

The government can increase budget expenditures and stimulate demand to promote production and business activities, thereby spurring credit demand and more vibrant activities in the credit market.

I would like to emphasise that the regulatory interest rate is just one factor in the operations of the credit market.

How can enterprises move towards exploiting the domestic market effectively, and taking advantage of the capital source considered abundant now?

The issue is that businesses should consider demands in the world and in domestic economies. According to our assessment, weak external demand, including from a subdued recovery in the China, hampered export-led manufacturing. The industrial production index shrank by 0.4 per cent in the first eight months of 2023, resulting in increased closures of businesses.

On average, 15,600 firms closed monthly, and hundreds of thousands of workers were laid off. The growth of industry and construction in aggregate dropped to 1.1 per cent in the first half of 2023.

On the domestic demand side, the recovery of domestic travel led consumption to grow by 2.7 per cent in the first six months of 2023. Investment, however, remained subdued in this period as gross capital formation growth declined to 1.2 per cent from 3.8 per cent a year earlier. Foreign direct investment disbursements were $10 billion in the first half of 2023, the same level as the previous year.

However, those foreign investment commitments in the period are estimated at $13.4 billion, down by 4.3 per cent on-year as a result of geopolitical tensions and tightened global financial conditions. Weak external demand worsened trade, impeding overall growth.

It would be challenging to increase export demand even though the government has made moves related to market opening, such as promoting free trade agreements or bilateral foreign relations.

However, these actions will take time for enterprises to land orders. Therefore, stimulating domestic demand will be the focus to support economic recovery.

Firstly, one of the most effective measures is to increase public investment and state budget spending. Secondly, with low savings interest rates, the public can reduce their motivation in saving money and thus increasing consumption.

When domestic demand strengthens, businesses will be able to boost their performance, although there may be a delay because they may still have to go reduce inventories before increasing production.

ADB sets moderate 2023 growth outlook for Vietnam

ADB sets moderate 2023 growth outlook for Vietnam

After a strong performance last year, the Vietnamese economy can expect moderate growth of 6.5 per cent this year, followed by a slight improvement to 6.8 per cent in 2024, according to a recent economic publication from the Asian Development Bank (ADB).

Variables still at play in global monetary policy

Variables still at play in global monetary policy

Le Xuan Nghia, director of the Business Development Institute and member of the National Financial and Monetary Policy Advisory Council, scrutinises the development prospects in Vietnam and around the world for the remainder of 2023 and beyond.

More harmonisation advised for fiscal and monetary policy

More harmonisation advised for fiscal and monetary policy

While the additional loosening of monetary policy is constrained, Vietnam should focus on boosting the expansion of fiscal policy to spur domestic production and business activities, economists have said.